June 26, 2026

Continuing the Struggle for Economic Competitiveness

By Brooke Thomson President & CEO When the Massachusetts Supreme Judicial Court disqualified a tax-reduction ballot question two…

Read MoreYvan Bodart, CFA | Managing Director

Kathy Sablone, JD, AEP® | Chief Planning Officer

On November 8, 2022, Massachusetts voters voted in favor of Massachusetts Ballot Question 1, often referred to as the “Millionaires’ Tax” or the “Fair Share Amendment.” Approval means that the Massachusetts State Constitution will be amended so that starting January 1, 2023, a 4% surtax will be imposed on any income over $1 million. This is in addition to the current flat rate of 5% that Massachusetts imposes on income.

The amendment does not limit the circumstances in which the new tax applies. Consequently, the additional 4% surtax will apply to taxpayers who regularly earn more than $1 million of annual income as well as “one-time” income millionaires. As such, events like the sale of a home or business can push a taxpayer into the 4% surtax threshold.

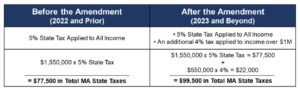

To further illustrate, let’s look at an example of an individual taxpayer with a recent home sale for $1.5 million

and a salary of $500,000:

In this example, the cost basis of the home was $200,000 and the individual has applied the personal residence exemption of $250,000, so the gain on this sale is $1,050,000. When the individual’s salary of $500,000 is added, their total income in that year would be $1,550,000, resulting in an extra 4% tax on the $550,000 in excess of $1 million. Relative to 2022, this would result in an additional $22,000 paid in state taxes:

While there are several aspects of the new tax law that require further clarification by the state, taxpayers should consider working with their advisors to implement new strategies in their portfolios, estate plans, and financial plans. Below we outline some of the steps that both one-time income millionaires and recurring $1 million income earners may wish to evaluate:

1. Immediately after the news that Question 1 had passed, some decided to accelerate income into 2022 before the new 4% surtax took effect. To the extent possible, this was achieved by recognizing capital gains, selling homes, and completing Roth conversions. In addition, taxpayers who anticipated

generating more than $1 million in income next year could benefit from delaying the realization of capital losses until 2023 when they might have a larger impact.

2. Going forward, where appropriate, investors may consider including income tax-free and income-minimizing investments in their portfolios, like municipal bonds and non-dividend paying securities.

3. Individuals over age 70 ½ can make qualified charitable distributions (QCD) from IRAs in lieu of Required Minimum Distributions (RMD). The amounts distributed to charity will not be included in taxable income. QCDs cannot exceed $100,000 per year.

4. Those who are still working may wish to maximize their pre-tax contributions to qualified plans such as a 401k. Business owners should evaluate their current plans with compensation planning consultants to determine whether any changes or enhancements would be beneficial.

5. Beginning in 2023, Massachusetts will allow charitable deductions against taxable income. As such, taxpayers with charitable intent will be able to offset some of the tax increase.

6. Interestingly, it appears that the amendment applies to income above $1 million on a per-return basis. Beginning in 2023, households that normally file joint returns should evaluate whether filing separately could be beneficial. This strategy assumes that the Massachusetts Department of Revenue does not introduce guidance prohibiting this practice. In addition, this may require transferring assets between spouses to shift income.

7. For those selling a business, installment payments that spread income across multiple tax years may reduce the impact of the surtax.

8. Taxpayers can make gifts to non-grantor irrevocable trusts. This will shift income and future appreciation out of taxable estates. This strategy has the added benefit of using the current Estate and Gift Tax Exemption before it is reduced when the Tax Cuts and Jobs Act of 2017 sunsets in 2026.

Boston Financial Management continues to monitor further developments, and we welcome any member of the Associated Industries of Massachusetts to reach out to Yvan Bodart or Kathy Sablone for guidance.